-

Initial Enrollment Period (IEP):

- When: The seven-month period that begins three months before your 65th birthday month and ends three months after.

- Who Qualifies: Individuals who are turning 65 and are eligible for Medicare based on age.

-

General Enrollment Period (GEP):

- When: January 1 to March 31 of each year.

- Who Qualifies: Individuals who didn’t enroll in Medicare during their Initial Enrollment Period and don’t qualify for a Special Enrollment Period (SEP). However, enrolling during this period may result in late enrollment penalties.

-

Special Enrollment Period (SEP):

- When: Throughout the year, depending on qualifying events.

- Who Qualifies: Individuals who experience certain life events, such as moving to a new area, losing employer coverage, or qualifying for Extra Help (low-income subsidy). Each event has specific eligibility criteria and timeframes for enrollment.

-

Annual Enrollment Period (AEP):

- When: October 15 to December 7 of each year.

- Who Qualifies: Individuals who are already enrolled in Medicare and want to make changes to their coverage. This includes switching from Original Medicare to a Medicare Advantage plan, switching between Medicare Advantage plans, or changing or adding a Part D prescription drug plan.

-

Medicare Advantage Open Enrollment Period (MA OEP):

- When: January 1 to March 31 of each year.

- Who Qualifies: Individuals who are already enrolled in a Medicare Advantage plan and want to make a one-time change. During this period, you can switch to a different Medicare Advantage plan or return to Original Medicare and add a Part D plan.

-

Medicare Part D Late Enrollment Penalty (LEP):

- When: Applies to individuals who delay enrolling in Medicare Part D (prescription drug coverage) when they are first eligible and don’t have creditable prescription drug coverage (coverage that is at least as good as Medicare’s).

- Who Qualifies: Individuals who have gone without creditable prescription drug coverage for 63 or more consecutive days after their Initial Enrollment Period.

-

Late Enrollment Penalties (LEPs) may apply if you don’t sign up for Medicare Part B or Part D when you are first eligible and don’t have other creditable coverage (coverage that is at least as good as Medicare’s). Here are the late enrollment penalties for Medicare Part B and Part D:

-

Medicare Part B Late Enrollment Penalty:

- Penalty Amount: The penalty is an additional 10% of the Part B premium for each full 12-month period that you could have enrolled in Part B but didn’t.

- Duration: The penalty is permanent and continues for as long as you have Medicare Part B.

-

Medicare Part D Late Enrollment Penalty:

- Penalty Calculation: The penalty is calculated by multiplying 1% of the national base beneficiary premium by the number of full, uncovered months you were eligible for Part D but didn’t enroll.

- Duration: The penalty is generally added to your Part D premium and remains in effect for as long as you have Medicare Part D. The specific penalty amount may vary depending on the length of time you were without creditable prescription drug coverage.

It’s important to note that the penalties can vary depending on your specific circumstances, and the actual penalty amounts are determined by Medicare. To get precise and personalized information about late enrollment penalties for your situation, it’s recommended to contact Medicare directly or consult with a licensed insurance agent who specializes in Medicare.

-

medicare

-

-

Premium: The amount you pay each month to be enrolled in Medicare or a Medicare plan. It’s like a subscription fee for your healthcare coverage.

-

Deductible: The amount you must pay out of pocket for healthcare services before Medicare starts to pay. Once you reach the deductible, Medicare will contribute its share towards the cost of your care.

-

Copayment: A fixed amount you pay for a healthcare service or prescription medication. For example, you might have a copayment of $20 for each doctor’s visit or a copayment of $10 for each prescription.

-

Coinsurance: The percentage of the cost of a healthcare service that you’re responsible for paying after reaching your deductible. For instance, if your coinsurance is 20%, you would pay 20% of the total cost, and Medicare would cover the remaining 80%.

-

Out-of-Pocket Maximum: The maximum amount you will have to pay for covered services in a calendar year. Once you reach this limit, Medicare will cover 100% of your healthcare costs for the rest of the year.

-

Original Medicare: The traditional fee-for-service Medicare program offered directly by the federal government. It includes Medicare Part A (hospital insurance) and Part B (medical insurance).

-

Medicare Advantage (Part C): Private insurance plans approved by Medicare that offer an alternative way to receive Medicare benefits. These plans often include additional benefits and may have provider networks.

-

Medicare Part D: Prescription drug coverage offered through private insurance companies approved by Medicare. Part D helps pay for the cost of prescription medications.

-

Medigap: Medicare Supplement Insurance plans sold by private insurance companies to help cover some of the costs that Original Medicare doesn’t pay, such as deductibles, copayments, and coinsurance.

-

Initial Enrollment Period (IEP): The seven-month period surrounding your 65th birthday when you are first eligible to enroll in Medicare. This is the best time to sign up to avoid potential late enrollment penalties.

-

Special Enrollment Period (SEP): A period outside the initial enrollment period when you can sign up for Medicare due to certain life events, such as losing employer coverage or moving to a new area.

-

Formulary: A list of prescription drugs covered by a Medicare Part D plan. Each plan has its own formulary, so it’s important to check if your medications are covered before choosing a plan.

-

Network: The group of doctors, hospitals, and other healthcare providers that have contracted with a specific Medicare Advantage plan or private insurance company to provide services to plan members.

-

Prior Authorization: The process of getting approval from Medicare or your insurance company before receiving certain healthcare services, medications, or procedures. It ensures that the treatment is medically necessary.

-

Annual Wellness Visit: A yearly appointment with your healthcare provider to create or update a personalized prevention plan based on your current health and risk factors. This visit is covered by Medicare at no cost to you.

-

Q: What is Medicare? A: Medicare is a health insurance program provided by the government for people who are 65 or older, certain younger individuals with disabilities, and those with end-stage renal disease.

Q: How is Medicare different from Medicaid? A: While both Medicare and Medicaid are government programs that assist with healthcare costs, Medicare primarily serves older adults and people with disabilities, regardless of income. Medicaid, on the other hand, is based on financial need and provides health coverage to low-income individuals and families.

Q: What are the different parts of Medicare? A: Medicare is divided into several parts:

- Part A: Hospital insurance that helps cover inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care.

- Part B: Medical insurance that helps cover doctor visits, outpatient care, preventive services, and medical supplies.

- Part C: Also known as Medicare Advantage, it offers an alternative way to receive Medicare benefits through private insurance companies.

- Part D: Prescription drug coverage that helps pay for prescription medications.

Q: When should I enroll in Medicare? A: If you’re already receiving Social Security benefits, you’ll be automatically enrolled in Medicare Parts A and B when you turn 65. If you’re not receiving Social Security benefits, you’ll need to proactively sign up during the Initial Enrollment Period (IEP), which begins three months before your 65th birthday and lasts for seven months.

Q: Do I need to pay for Medicare? A: While most people do not pay a premium for Medicare Part A (if they have paid Medicare taxes while working), there are premiums associated with Medicare Part B and Part D. The amount you pay depends on your income and the plan you choose.

Q: Can I have other insurance along with Medicare? A: Yes, it’s possible to have other insurance alongside Medicare. Many people choose to get additional coverage through a Medicare Supplement Insurance (Medigap) policy to help pay for costs that Medicare doesn’t cover. Others opt for Medicare Advantage plans that provide both Medicare Parts A and B coverage, often with prescription drug coverage as well.

Q: What does Medicare not cover? A: Medicare doesn’t cover everything, and there are gaps in coverage. Some examples of services not covered by Medicare include long-term care, most dental care, eye exams for glasses, hearing aids, and cosmetic surgery.

Q: Can I change my Medicare coverage? A: Yes, there are specific periods when you can change your Medicare coverage. The Annual Enrollment Period (AEP) occurs each year from October 15 to December 7, during which you can switch between Medicare Advantage and Original Medicare, change or add a Part D plan, or move from one Part D plan to another.

Q: How do I find doctors who accept Medicare? A: You can find doctors who accept Medicare by using the “Physician Compare” tool on the official Medicare website or by contacting the doctor’s office directly and asking if they accept Medicare patients.

Q: What if I need help understanding Medicare or making decisions? A: If you need assistance understanding Medicare or making decisions about your coverage, you can contact your State Health Insurance Assistance Program (SHIP) or speak with a licensed insurance agent who specializes in Medicare.

Last Updated: January 11th, 2025

What you need to know about Medicare’s Open Enrollment Period (OEP)

What changes can you make during OEP?

Medicare, a crucial lifeline for millions of Americans, is a comprehensive health insurance program designed to provide coverage for individuals aged 65 and older or those with certain qualifying disabilities. While many are familiar with the initial enrollment period, there’s another important phase called the Open Enrollment Period (OEP) that deserves attention. In this blog post, we’ll explore what the OEP is, who qualifies, why it’s important, and other topics that can benefit Medicare beneficiaries.

The Open Enrollment Period (OEP) is a specific time frame when Medicare beneficiaries can change their coverage. OEP takes place every year from January 1st to March 31st. You can change your Medicare policy during this period, also known as the Medicare Advantage Open Enrollment Period.

What is the Open Enrollment Period (OEP)?

Each year from January 1st until March 31st, you can switch your Medicare plan if enrolled in a Medicare Advantage Plan. During OEP you can make the change from a Medicare Advantage plan to a different one or to Original Medicare. It is important to know that you can only change plans once during this period.

If you recently turned 65 and were too late enrolling into Medicare during your initial period (when you were first eligible; 3 months before and after you turned 65) you can use the Medicare General Enrollment Period (GEP) to enroll in a Medicare part A and/or B plan. GEP also starts on January first – March 31st. You might qualify for a Special Medicare Enrollment Period (SEP), If you missed your initial enrollment period and had creditable coverage. For more information you can read our other blog about what to do if you missed your Medicare enrollment period.

What changes can you make during OEP?

Medicare beneficiaries who are already enrolled in Medicare Advantage (Part C) or Medicare Prescription Drug Plans (Part D) can participate in the OEP. If you have Original Medicare (Part A and/or Part B), you cannot make changes during the OEP; however, you have other opportunities for adjustments.

What is possible during OEP?

- You can Switch to a different type of Medicare Advantage plan (Part C).

- You can Drop your Medicare Advantage plan and go back to having an Original Medicare plan (Parts A & B).

- You can Enroll in a Medicare prescription drug plan (Part D) if you want to go back to an Original Medicare plan

What is not possible during OEP?

- You can’t switch from Original Medicare to a Medicare Advantage Plan.

- You can’t add a Medicare drug plan if you’re in Original Medicare.

- You can’t change your Medicare drug plan to another if you’re in Original Medicare.

Why is OEP important?

The OEP is essential because it allows beneficiaries to review and modify their existing coverage to better suit their healthcare needs. Here are a few reasons why the OEP is significant:

a. Changes in Health Needs: Your health needs may evolve over time, and the OEP provides a chance to adjust your coverage accordingly.

b. New Plan Offerings: Insurance providers may introduce new plans or alter existing ones. The OEP lets you explore these options and switch plans if necessary.

c. Prescription Drug Changes: Medication needs can change, and the OEP enables beneficiaries to find a plan that covers their current prescriptions at the most affordable rates.

")

Do I have to enroll in Medicare every year?

It is not required to make any changes to your Medicare coverage every year. If you are happy with your plan, you can keep it.

However, reviewing your plan every year is wise to ensure it meets your needs and that you are not overpaying for your policy.

A different Medicare plan in your area could offer better provider networks, lower costs, a more extensive range of coverage, or other benefits that make the plan a better fit for you.

Other Tips for Medicare Beneficiaries:

a. Review Your Annual Notice of Change (ANOC): Insurance providers send an ANOC each fall, detailing any changes to your plan’s costs, benefits, or rules for the upcoming year.

b. Utilize Available Resources: Take advantage of online tools and resources provided by Medicare, such as the Plan Finder tool, to compare plans and find the best fit for your needs.

c. Consider Additional Coverage: Explore options

What is the difference between Medicare’s Annual Enrollment Period (AEP) and OEP ?

OEP: is from January 1st–March 31st.

Your new coverage will start the first day of the month after you ask to enroll in the plan.

During OEP, you can.

- You can Switch to a different Medicare Advantage plan (Part C).

- You can Drop your Medicare Advantage plan and return to having an Original Medicare plan (Parts A & B).

- You can Enroll in a Medicare prescription drug plan (Part D) if you want to return to an Original Medicare plan.

What is the Annual Election Period?

AEP: From October 15th – December 7th.

During the Medicare Annual Enrollment Period (AEP), you make specific changes to your Medicare Advantage (Part C) or Medicare prescription drug (Part D) plan.

You can make the following changes during AEP (Medicar.gov):

- Switch from Original Medicare to a Medicare Advantage Plan.

- Switch from a Medicare Advantage Plan back to Original Medicare.

- Change from one Medicare Advantage Plan to another Medicare Advantage Plan.

- Change from a Medicare Advantage Plan that doesn’t offer drug coverage to a Medicare Advantage Plan that offers drug coverage.

- Change from a Medicare Advantage Plan that offers drug coverage to a Medicare Advantage Plan that doesn’t offer drug coverage.

- Add on a Medicare drug plan.

- Change from one Medicare drug plan to another Medicare drug plan.

- Drop your Medicare drug coverage altogether.

Need to review your Medicare plan?

Last Updated: February 5th, 2026

Missed the Medicare Enrollment Deadline?

You might still have a chance to avoid the penalties.

Timing is everything! Generally, if you miss an enrollment deadline, you will need to wait until the general enrollment period (GEP) and most likely pay the penalty. However, there are special enrollment periods (SEP) you might qualify for. If you do, you may avoid paying penalties. This means you can sign up outside our initial enrollment period, which starts three months before you turn 65 and lasts up to three months after.

When do you qualify for the special enrollment period?

Employment.

If you or your spouse still work(s), and you have health insurance through either of your employers.

- You can still sign up for Medicare part A, most people don’t have to pay a premium, and it will cover hospital expenses. You won’t have to pay a premium if Medicare taxes are deducted from your or your spouse’s paychecks for at least ten years.

Missed the deadline? No worries, you might be able to delay your enrollment without having to pay for any penalties. Depending on your plan through work, you may not need to enroll in Medicare part B or D. If you do have creditable coverage through work, keep the Certificate of Creditable Coverage in your records as proof. You will likely need to use this as proof that you had creditable coverage later. Plan to enroll before your employer coverage ends to avoid penalties due to a gap in your coverage.

For Part B, you’ll need to sign up before your employer coverage ends or within eight months of losing your job-based coverage to avoid a late-enrollment penalty.

For Part D, you’ll have a shorter special enrollment period — two months after the month that your previous prescription drug coverage ends.

When your employment-based health insurance ends, you can sign up for Part B during the special enrollment period. After that, you can sign up for a Part D prescription drug policy and a Medigap policy, covering most of Medicare’s deductibles and copayments. You could also purchase a private Medicare Advantage plan, which provides medical and drug coverage.

Click here to learn more about if it’s better to keep your employer’s coverage or enroll in Medicare

When should you enroll in Medicare to avoid penalties?

Medicare’s sign-up window starts three months before your birth month when you turn 65 and ends three months after. You will have to enroll in Medicare during this sign-up window to avoid penalties unless you have creditable coverage (ex., employer health insurance plan).

You will have guaranteed issue rights during your initial enrollment period; insurance companies can’t deny you a Medicare Supplement insurance plan because of pre-existing health conditions or disabilities.

Late Enrollment Penalty part B: Your monthly Part B premium could be 10% higher for every entire 12-month period that you were eligible for Part B.

That means one year is 10%, two years is 20%, three years is 30%, and so on.

For each month you delay enrollment in Medicare Part D, you will have to pay a 1% Part D late enrollment penalty (LEP). The penalty is calculated based on 1% of that year’s national average Part D monthly cost. For example, the national average for 2026 is $38.99, so if you went 12 months without credible prescription coverage, your penalty would be as follows:

$38.99 x 1% = $4.70 penalty per month.

We Are Here To Help

Enrollment period overview

- Initial Enrollment Period: Lasts for seven months; your sign-up window is from 3 months before your birth month when you turn 65 to 3 months later. You have to enroll in Medicare during this sign-up window to avoid potential penalties. If you don’t register in time, you may have to pay the penalty for parts B and D.

-

Medicare Annual Enrollment Period (AEP): Anyone can use the AEP to make changes to their Medicare coverage – from October 15 to December 7

- Open Enrollment Period: January 1 to March 31

- Lock-in Period: April 1 to December 31

- Special Enrollment Period: Special circumstances within the year

-

Medicare Birthday Rule: The Medicare birthday rule allows consumers to change to an equal or lesser Medigap policy

within a 60-day window without medical underwriting (not available in all states).

Click here to learn about the steps you need to take to sign up for Medicare

Medicare published some of the new Medicare costs for 2023. This includes the new part B premium and the Part B deductible. There is some good news; the new premium for part B will drop to $164.90 in 2023 ($170.10 in 2022), and the deductible for Part B will also decrease.

Overview Medicare updates 2023

- Part A premiums, deductibles, and coinsurance also increased in 2023.

- Medicare’s Part B standard premium & deductible decreased for 2023.

- Medicare’s Part B and D income brackets for high-income premium adjustments start at $97,000 for a single person,

and the high-income adjustment amount for Part B and Part D decreased in 2023. - Beginning January 1, 2023, Medicare will offer a new benefit that helps you continue to pay for your immunosuppressive drugs beyond 36 months.

Medicare part B dropped in price!

Medicare Part B:

It covers services from doctors and other health care providers, certain home health services, and other medical and health services not covered by Medicare Part A.

In 2023 the new standard monthly premiums for Medicare part B will be $164.90. The deductible for 2023 also decreased from $233 to $226. You will be paying this deductible if you have a Medicare supplement plan that doesn’t cover the deductible (for example, plans G & N).

Medicare gave the following reasons for the price drop (CMS); there was lower spending than projected on part B services, which resulted in much larger reserves. The excess SMI (Supplementary Medical Insurance) reserves are passed along to people with Medicare Part B coverage (price drop).

Medicare Part A:

Gives coverage for inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care.

Deductible

$1.600 (was $1,556 in 2022) for each inpatient hospital benefit period before Original Medicare starts to pay.

Inpatient stay

Days 1-60: $0 after you pay your Part A deductible.

Days 61-90: $400 copayment each day (was $389 in 2022).

Days 91-150: $800 copayment each day while using your 60 lifetime reserve days ($778 in 2022).

After day 150: You pay all costs.

.

.

Skilled nursing facility stay

Days 1-20: $0 copayment.

Days 21-100: $200 copayment each day (was $194.50 in 2022).

Days 101 and beyond: You pay all costs.

– source medicare.gov

What about immunosuppressive drugs in 2023?

Starting in 2023, some Medicare enrollees who are past the 36th month of a kidney transplant are no longer eligible for full medicare coverage. Instead, they can elect to continue Part B coverage of immunosuppressive drugs by paying a premium. This premium will cost $97.10. Learn more about this on page 52.

These are the published changes so far; we will continue to update the blog when more information is released.

Medicare 101 Webinar

We also host an Educational Medicare 101 webinar every week.

During this webinar, you will:

- Learn about how changes in the 99+ plans in your area will affect your next year by attending this Medicare Annual Election Period educational seminar.

- How to decide whether a Medicare Supplement or Medicare Advantage Plan is right for you based on your needs.

- How to avoid the top 7 reasons people overspend by thousands of dollars each year.

- How to take advantage of specific rights & entitlements that protect you from overpaying

Last Updated: January 11th, 2025

The Best Time to Start Receiving Social Security Benefits:

A Comprehensive Guide for Retirees

Social Security is a crucial supplemental income source during retirement, and the timing of when to start receiving benefits can significantly impact your financial well-being. This blog aims to help retirees make informed decisions by exploring the three common scenarios: stopping work before retirement age, continuing to work while receiving benefits, and working without receiving retirement benefits. We will delve into each situation’s key points, benefits, and considerations, ensuring you can choose the best time to receive Social Security benefits.

Social Security is one of the few supplemental income sources during retirement that changes yearly for inflation. Deciding whether you should wait to receive Social Security benefits is essential. If you choose to start your benefits before your full retirement age, your benefits will likely be reduced at a fraction of a percent for every month before you reach the full retirement age. It might be better to wait until you reach full retirement age or delay it more to receive an increase in Social Security benefits.

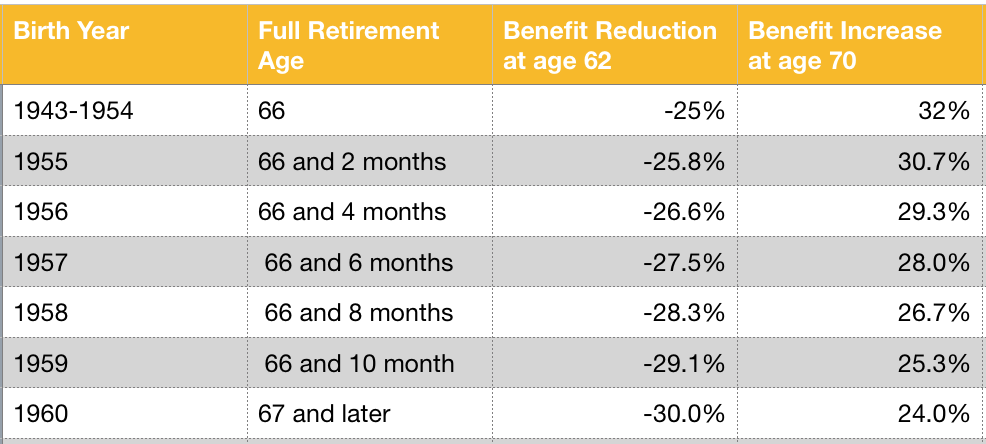

According to Social Security Administration, based on data from 2022, your full retirement age =

* 66 years and four months (if born in 1956)

* 67 years for those born in 1955 and beyond.

Situation A

Stopping Work Before Retirement Age & Starting Social Security Benefits

If you are considering retiring early and starting to receive Social Security benefits, there are essential factors to consider. You can apply for Social Security benefits as early as age 62, but doing so will result in reduced benefits. The reduction amounts to 6% per year or 0.5% per month (as of 2022) for each month you receive benefits before reaching your full retirement age. On the other hand, if you delay receiving benefits, you may qualify for an increase of 8% per year or 0.67% per month until you reach the age of 70.

Key Points:

- You can apply for Social Security Benefits as early as age 62

- If you apply before reaching your full retirement age, your benefits will be reduced by 6% per year or 0.5% per month (2022), and if you delay, it’s an 8% per year deferral credit or 0.67% per month.

It’s crucial to weigh the trade-offs carefully. While starting benefits early can provide additional income, waiting until your full retirement age or beyond can result in higher benefit amounts for the rest of your life. For instance, delaying benefits until age 70 can yield up to 33% higher benefits compared to taking them at full retirement age, as shown in Table 1.

You will automatically enroll in Original Medicare (Part A and Part B) when you turn 65.

Table 1, 2020 What your Social Security reduction would be if you applied at age 62 compared to an increase at age 70

If you decide to work after receiving Social Security benefits, your benefit payments will be recalculated based on that year’s income limits. Additionally, at age 65, you will automatically enroll in Original Medicare (Part A and Part B).

Situation B

Continuing Work and Receiving Social Security Benefits

Retirees who wish to keep working while receiving Social Security benefits can do so, but certain income limits may affect the benefits they receive. If you are younger than your full retirement age during the tax year, the income limit is $22,320 in 2024. For every $2 you earn above this limit, $1 will be deducted from your Social Security benefits. Once you reach your full retirement age, the income limit increases to $59,520, and the reduction changes to $1 in benefits for every $3 you earn above the limit.

However, it’s essential to understand that the income limits only apply to income earned through work and not other sources such as investments, annuities, pensions, or capital gains. Moreover, there are no reductions in benefits if you work after reaching your full retirement age.

Key Points:

- You can work and receive Social Security benefits.

- Your Social Security benefits will be reduced until you reach full retirement age.

- The maximum income you can earn to avoid an extra benefit reduction depends on how close you are to the full retirement age. If your income is above this limit, they will reduce your benefits until you reach full retirement age.

- Double penalty – if you earn more than the income limit, apply before full retirement age.

- There are no reductions if you work after you reach your full retirement age.

Can you work and receive Social Security benefits?

Yes, you can work and get Social Security benefits simultaneously. Social Security can give you the extra boost of income you need if your job doesn’t give you enough. However, there are income limits. They will deduct a certain amount from your benefits if you earn more than these limits. The income limits only apply to income from work, and it does not count for investments, annuities, pensions, or capital gains.

What are the Income Limits for 2024?

The Social Security Administration sets its income limits for people receiving Social Security benefits yearly. This is the amount you are allowed to earn without getting a reduction on your Social Security payments. If you make more than the limit ($22,320 in 2024), your benefits will be reduced (if you are younger than the retirement age). Luckily, these reductions will be returned to you when you reach full retirement. The social security benefits are only withheld temporarily.

If you’re younger than full retirement age during all of 2024, they will deduct $1 from your benefits for each $2 you earn above $22,320. If you reach full retirement that year, the limit changes to $59,520 (2024). They will deduct $1 in benefits for every $3 you earn above the limit.

If you are older than full retirement and decide to work, you will receive your full benefits; there are no income limits.

For more examples, visit ssa.gov.

*note: there are different rules if you work outside the country or are on disability.

You will automatically enroll in Original Medicare (Part A and Part B) when you turn 65. Check before signing up for Medicare Part B if you or your spouse are still covered under an employer-provided group health plan.

Situation C

Continuing Work and Delaying Social Security Benefits

There can be significant advantages for retirees who choose to keep working and delay receiving Social Security benefits. For each month you delay your benefits beyond your full retirement age, your benefits increase. Delaying until age 70 can lead to the maximum possible increase in benefits, up to 33% more than what you would receive at your full retirement age (see Table 1). Furthermore, delaying Social Security benefits can be beneficial since your current earnings may replace earlier years of lower or no wages, leading to a higher benefit amount. However, keep in mind that enrolling in Original Medicare (Part A and Part B) three months before turning 65 is crucial to avoid penalties if you do not receive your Social Security benefits at that time.

Key Points:

- If you decide to keep working and not start your benefits until after your full retirement age, your benefits will increase for every month you do not receive them until you reach the age of 70.

- Delaying can also increase your benefits because your current earnings could replace an earlier year of lower or no wages.

*You will need to enroll in Original Medicare (Part A and Part B) three months before you turn 65 to avoid any penalties if you don’t receive your Social Security benefits when you turn 65

How much will you get?→Social Security Quick Calculator

Want to learn more?

Deciding when to start receiving Social Security benefits is a critical financial decision that can significantly impact your retirement income. Each situation has its merits and drawbacks, and understanding the implications of starting early, continuing to work, or delaying benefits is crucial. By carefully assessing your financial needs, health status, and long-term goals, you can make an informed choice that aligns with your unique circumstances.

Feel free to schedule a meeting with one of our licensed financial planners if you need help deciding when to apply for social security benefits or retirement planning in general; identifying goals and objectives is key to a successful retirement.

How to Avoid Medicare Part B & Part D Late Enrollment Penalties in 2026

Missing your Medicare enrollment deadline can lead to higher premiums for years. Understanding when to enroll and what coverage qualifies can help you avoid costly penalties and make more informed Medicare decisions.

Medicare Penalty Calculator

Estimate your Medicare Part B and Part D penalties instantly.

Part B Penalty

Monthly Penalty: $0.00

Part D Penalty

Monthly Penalty: $0.00

Understanding Medicare Enrollment Deadlines

Many Americans assume Medicare enrollment is automatic or that they can sign up whenever they choose. In reality, delaying enrollment without qualifying coverage may result in permanent premium penalties.

Key Insight: Medicare late enrollment penalties are often avoidable when you understand your enrollment deadlines and coverage options before turning 65. Most people become eligible for Medicare at age 65. Your Initial Enrollment Period (IEP) spans seven months:

3 Months Before Your Birthday Month → Birthday Month → 3 Months After Your Birthday Month

For many individuals, this is the simplest opportunity to enroll in Medicare without penalties. Missing this window may result in delayed coverage and higher premiums if you do not have qualifying employer-sponsored coverage.

Not Sure When You Should Enroll?

Schedule a Medicare review to understand your timeline.

Schedule Your Free Medicare ReviewMedicare Part B Late Enrollment Penalty

Medicare Part B covers physician services, outpatient care, preventive services, and durable medical equipment.

2026 premium: $202.90 per month

Part B Penalty Formula

10% increase for every 12 months delayed

| Delay Period | Penalty |

|---|---|

| 1 Year | 10% |

| 2 Years | 20% |

| 3 Years | 30% |

Example of Part B Penalty

Let’s say you delayed enrolling for 2 full years:

- Base premium: $202.90

- Penalty: 20%

- Monthly increase: $40.58

- New premium: $243.48/month

Important: This penalty often lasts as long as you have Part B.

Medicare Part D Late Enrollment Penalty

Medicare Part D helps cover prescription drugs.

Part D Penalty Formula

1% × National Base Premium × Months Uncovered

For 2026, the National Base Beneficiary Premium is $38.99.

Example of Part D Penalty

Example: 18 months without coverage

- $38.99 × 1% = $0.3899

- $0.3899 × 18 = $7.02/month

Important: Even small gaps can create lifelong penalties.

What Counts as Creditable Coverage?

Creditable coverage is insurance that Medicare considers at least as good as standard Medicare coverage.

| Typically Creditable | May Not Protect |

|---|---|

| Employer Coverage | COBRA |

| Union Coverage | Some Retiree Plans |

| TRICARE | Marketplace Plans |

Common Medicare Enrollment Mistakes

- Assuming Medicare is automatic. Not everyone is automatically enrolled.

- Relying on COBRA. COBRA coverage may not protect against Part B penalties.

- Skipping Part D because you take few prescriptions. Penalties can still apply.

- Missing employer coverage rules. Employer size and plan structure can affect enrollment decisions.

Special Enrollment Periods (SEP)

Some individuals qualify for a Special Enrollment Period that allows Medicare enrollment without penalties.

Common examples include:

- Continuing to work beyond age 65 with qualifying employer coverage

- Losing employer-sponsored coverage

- Certain exceptional circumstances recognized by Medicare

Eligibility for a Special Enrollment Period depends on individual circumstances and Medicare rules in effect at the time of enrollment.Avoid Costly Medicare Mistakes

Review your enrollment timeline, current coverage, and Medicare options with a licensed Medicare Insurance agent.

Schedule Your Medicare ReviewFrequently Asked Questions

Is the Medicare Part B penalty permanent?

In many cases, the Part B late enrollment penalty remains for as long as you have Part B coverage.

How is the Part D penalty calculated?

The penalty is generally calculated as 1% of the national base beneficiary premium for each month you lacked creditable prescription drug coverage.

Can I delay Medicare if I am still working?

Possibly. Individuals with qualifying employer-sponsored coverage may be eligible to delay enrollment without penalties.

Does COBRA count as creditable coverage?

COBRA may provide health insurance coverage, but it does not always protect against Medicare late enrollment penalties.

Disclosure: This material is for educational purposes only and should not be considered tax, legal, insurance, or financial advice. Individual situations vary, and Medicare rules may change. Consult appropriate professionals regarding your specific circumstances.

How to Avoid Medicare Part B & Part D Late Enrollment Penalties

The best way to avoid Medicare penalties is not complicated, but it does require understanding your enrollment timeline and making sure you don’t miss key deadlines.

1. Enroll During Your Initial Enrollment Period (IEP)

Your Initial Enrollment Period (IEP) is your primary opportunity to enroll in Medicare without penalties. It lasts 7 months total:

- 3 months before your 65th birthday month

- Your birth month

- 3 months after your birth month

Enrolling in Medicare Part A, Part B, and Part D during this window typically helps you avoid late enrollment penalties altogether.

2. Make Sure You Have “Creditable Coverage” If You Delay

If you continue working past age 65 and remain on employer coverage, you may be able to delay Medicare without penalties—but only if your coverage is considered creditable.

- Employer has 20+ employees (in most cases)

- Coverage is as good as or better than Medicare

- Prescription drug coverage meets Medicare creditable standards

If your coverage is not creditable, delaying enrollment may result in permanent penalties.

3. Use a Special Enrollment Period (SEP) When You Qualify

A Special Enrollment Period (SEP) allows you to enroll in Medicare after your IEP without penalties if you had qualifying coverage.

- Losing employer or union coverage

- Retiring and losing group health insurance

- Moving outside your plan’s service area

- Other qualifying life events

In most cases, you must enroll within a specific timeframe after losing coverage to avoid penalties.

4. Don’t Assume COBRA or Retiree Coverage Protects You

One of the most common mistakes is assuming COBRA or retiree coverage will prevent penalties.

- COBRA generally does not count as creditable coverage for delaying Part B

- Retiree plans may not meet Medicare requirements

- You may still be required to enroll when first eligible

5. Avoid Coverage Gaps Longer Than 63 Days (Part D Rule)

For Medicare Part D, penalties apply if you go 63 days or more without creditable prescription drug coverage after your initial eligibility period.

- Maintain continuous drug coverage whenever possible

- Enroll in Part D within 63 days of losing coverage

Even a short gap can result in a lifelong monthly penalty.

6. When in Doubt, Verify Before You Delay

Before delaying Medicare enrollment, confirm:

- Whether your employer coverage is creditable

- Whether your drug coverage meets Medicare standards

- Your exact enrollment timeline (IEP or SEP)

A quick verification can help you avoid permanent penalties that last for life.

Medicare Enrollment Periods: Understanding Your Windows to Enroll

Missing a Medicare enrollment deadline can result in delayed coverage and, in some cases, late enrollment penalties that may continue for as long as you have Medicare coverage. Understanding when you can enroll—and what options are available if your circumstances change—can help you avoid unnecessary costs and coverage gaps.

Important: Medicare enrollment rules vary depending on your age, employment status, health coverage, and eligibility circumstances. Reviewing your options before a coverage change occurs may help reduce the risk of enrollment delays or penalties.

Initial Enrollment Period (IEP)

Your Initial Enrollment Period is the first opportunity most people have to enroll in Medicare. This enrollment window lasts seven months and begins three months before the month you turn 65, includes your birth month, and continues for three months afterward.

For many individuals, this is the most important Medicare enrollment period because enrolling during this window may help avoid future Part B and Part D late enrollment penalties. If you miss your Initial Enrollment Period and do not qualify for a Special Enrollment Period, you may need to wait for another enrollment opportunity.

Common Mistake: Many individuals assume they are automatically enrolled in all parts of Medicare. While some people are automatically enrolled in Part A and Part B, others must actively enroll to avoid delays in coverage.

Annual Enrollment Period (AEP)

The Annual Enrollment Period runs from October 15 through December 7 each year. During this period, Medicare beneficiaries can review and make changes to their coverage for the following year.

- Switch from Original Medicare to a Medicare Advantage plan

- Switch from one Medicare Advantage plan to another

- Join, change, or leave a Part D prescription drug plan

- Return from Medicare Advantage to Original Medicare

Coverage changes made during the Annual Enrollment Period generally become effective January 1 of the following year.

Medicare Advantage Open Enrollment Period (OEP)

From January 1 through March 31, individuals already enrolled in a Medicare Advantage plan have an opportunity to make certain coverage changes.

- Switch to another Medicare Advantage plan

- Return to Original Medicare

- Add a standalone Part D prescription drug plan if returning to Original Medicare

This enrollment period is available only to beneficiaries currently enrolled in a Medicare Advantage plan.

Lock-In Period

Generally, from April 1 through December 31, Medicare beneficiaries remain enrolled in their existing coverage unless they qualify for a Special Enrollment Period or another Medicare-approved election opportunity.

Because plan changes may be limited during this time, it is important to carefully review your coverage during enrollment periods when changes are allowed.

Special Enrollment Period (SEP)

Special Enrollment Periods allow eligible individuals to enroll in Medicare or make coverage changes outside the standard enrollment periods due to qualifying life events.

Examples may include:

- Losing employer-sponsored health coverage

- Moving outside your current plan’s service area

- Changes involving Medicaid eligibility

- Qualifying for certain assistance programs

- Other Medicare-approved special circumstances

Eligibility requirements vary depending on the event and circumstances.

Medicare Birthday Rule

Certain states provide a Medicare Birthday Rule that may allow eligible individuals to switch Medicare Supplement (Medigap) plans without medical underwriting during a limited annual window.

Availability, eligibility requirements, and plan restrictions vary by state. In many cases, changes are limited to plans with equal or lesser benefits than your current Medicare Supplement plan.

Not Sure Which Enrollment Period Applies to You?

Understanding Medicare enrollment deadlines can be challenging, especially when employer coverage, retirement timing, COBRA, or disability benefits are involved.

A Medicare review can help identify upcoming deadlines, determine whether your current coverage is creditable, and explore available Medicare options based on your situation.

Schedule Your Free Medicare ReviewTips to Help Avoid Medicare Part B and Part D Penalties

Understand Your Enrollment Timeline

Knowing when your Medicare enrollment window begins and ends is one of the most effective ways to avoid penalties. Many late enrollment penalties occur simply because individuals are unaware of the deadlines that apply to their circumstances.

Enroll When First Eligible (If Appropriate)

For many individuals, enrolling during the Initial Enrollment Period may help avoid future penalties. However, those who have qualifying employer coverage may have different enrollment options. Review your situation carefully before delaying enrollment.

Review Employer Coverage Carefully

If you continue working past age 65 and have health insurance through an employer, determine whether your coverage is considered creditable for Medicare purposes. Not all employer-sponsored plans are treated the same under Medicare rules.

Keep Documentation

Maintain records of employer coverage, Certificates of Creditable Coverage, and enrollment paperwork. These documents may be necessary if Medicare requests proof that you maintained qualifying coverage.

Review Prescription Drug Coverage Annually

If your prescription drug coverage changes or you leave employer-sponsored coverage, your Medicare Part D enrollment options may also change. Annual reviews can help ensure your coverage remains appropriate.

Consider Medicare Advantage Carefully

Some Medicare Advantage plans include prescription drug coverage. Depending on your circumstances, enrolling in a plan that includes drug coverage may eliminate the need for a separate Part D plan. Coverage, provider networks, and drug formularies vary by plan.

Annual Review Reminder: Medicare plans, prescription formularies, provider networks, premiums, and benefits can change each year. Reviewing your coverage annually may help identify changes that could affect your healthcare costs.

Frequently Asked Questions About Medicare Late Enrollment Penalties

What If I Have Creditable Coverage Through Work or My Spouse’s Employer?

Depending on your employer-sponsored plan, you may be able to delay Medicare Part B and Part D enrollment without penalties. It is important to retain all Certificates of Creditable Coverage and related documentation for future reference.

When employer coverage ends due to retirement, job changes, or other circumstances, enrollment deadlines may apply. Planning ahead can help minimize the risk of coverage gaps.

What Happens If I Lose Creditable Coverage?

When qualifying coverage ends, Medicare enrollment deadlines begin. Delaying enrollment beyond available enrollment periods may result in late enrollment penalties depending on your circumstances and the length of the coverage gap.

Individuals leaving employer-sponsored coverage should review Medicare enrollment requirements before coverage terminates whenever possible.

Important: Coverage gaps can lead to delayed enrollment opportunities and may result in additional healthcare costs. Consider reviewing Medicare options before your existing coverage ends.

How Does COBRA Affect Medicare Enrollment?

COBRA coverage and Medicare enrollment rules can be complex. While COBRA may provide temporary continuation coverage, it is not always treated the same as active employer coverage for Medicare enrollment purposes.

Individuals considering COBRA should understand how it coordinates with Medicare and what enrollment deadlines may apply. Delaying Medicare enrollment while relying solely on COBRA may create future penalties or coverage gaps in certain situations.

COBRA coverage is generally available for up to 18 months, although longer periods may apply under specific circumstances.

What If I Qualify for Medicare Due to Disability?

Individuals receiving Social Security Disability Insurance (SSDI) may become eligible for Medicare before age 65. Medicare enrollment decisions should be evaluated carefully because disability-based eligibility can differ from age-based eligibility.

When a disability beneficiary later turns 65, a new Medicare Initial Enrollment Period generally begins based on age eligibility. This creates an opportunity to review Medicare coverage options again.

How Do Disability and Guaranteed Issue Rights Work?

Certain individuals becoming eligible for Medicare may qualify for Guaranteed Issue rights, which can provide access to Medicare Supplement insurance without medical underwriting during specified enrollment periods.

Guaranteed Issue rights vary based on state rules, eligibility status, and enrollment timing. Availability should be verified based on your specific situation.

Need Help Avoiding Medicare Enrollment Penalties?

Whether you’re turning 65, retiring, losing employer coverage, or evaluating Medicare plan options, understanding your enrollment timeline is an important part of making informed Medicare decisions.

Our Medicare planning team can help you review enrollment periods, creditable coverage requirements, Medicare Supplement options, Medicare Advantage plans, and prescription drug coverage.

Schedule Your Free Medicare ReviewImportant Disclosure

This information is provided for educational purposes only and should not be considered legal, tax, financial, or Medicare advice. Medicare rules, enrollment periods, and penalties are subject to change. Individual circumstances vary. Consult Medicare, your employer benefits administrator, or other qualified professionals regarding your specific situation.

Last Updated: January 11th, 2025

Retirement Planning & Long-term Care

Long-term care is often overlooked, and the costs are underestimated in retirement planning. On top of that, long-term care expenses are growing every year. The possibility of needing help taking care of yourself later in life is probably hard to imagine and most likely not on your priority list. However, if you forget to add this to your planning, you might run out of your retirement savings before you know it.

Why is it important to plan for long-term care?

As we journey through life, it’s essential to consider our present needs and potential challenges that may arise in the future. Long-term care is a crucial aspect that often gets overlooked until it becomes an immediate concern. Research indicates that an astounding 70% of individuals over 65 will require some form of long-term care in their lifetime (acl.gov). Therefore, proactive planning for long-term care is not only wise but necessary to ensure a worry-free and secure future. In this blog, we will delve into the significance of preparing for long-term care and explore various options that can help you navigate this complex terrain.

Ask yourself the following question;

If you need long-term care, how will you pay for it, or who will pay for it?

The Reality of Long-Term Care Costs: Before we dive into the planning options, let’s first understand the magnitude of long-term care expenses. According to the median cost survey conducted by Genworth in 2022, here’s an overview of the average annual costs for various care options:

- In-home homemaker services: $53,768

- In-home health aide: $54,912

- Community adult day care: $19,240

- Community assisted living facility: $51,600

- Nursing home semi-private room: $93,075

- Nursing home private room: $105,850

Based on the numbers, it’s clear that long-term care can have a major impact on your financial stability if you don’t plan for it properly.

What about Health Insurance and Medicare?

While many individuals may assume that their regular health insurance or Medicare will cover long-term care costs, this is unfortunately not the case. Medicaid can provide assistance if your income falls within the Medicaid income limits. However, relying solely on Medicaid might restrict your choices for care, limiting the options for location and type of care you receive. Early planning is, therefore, essential to ensure you have the freedom to make informed decisions about your long-term care preferences.

Please plan and be ready in case you need it

There are different ways to prepare for these costs, and they all have ups and downs. We will discuss five options.

Option 1: Long-term care insurance

Long-term care insurance is a reliable option that offers peace of mind for the future. People opt for this type of insurance for two primary reasons:

-

Protecting Retirement Savings: Long-term care insurance shields your hard-earned retirement savings from being depleted by exorbitant care expenses.

-

Choice and Flexibility: With long-term care insurance, you can choose the type of care you desire, be it in your home, an assisted living facility, adult daycare center, hospice care, memory care, or nursing home care.

This insurance covers not only routine daily activities like bathing and dressing but also chronic medical conditions, disabilities, and disorders. While the policy price may increase in the future, the benefits far outweigh the potential drawbacks. The cost of the policy can be influenced by factors such as age, the maximum amount it pays per day, the number of years it will pay, and optional benefits like inflation protection.

What does long-term care insurance cover?

Long-term care insurance not only covers the basic routine daily activities, like bathing, dressing, or getting in and out of bed, but it will also cover in case of a chronic medical condition, a disability, or a disorder.

- Your home.

- An assisted living facility.

- An adult daycare center.

- Hospice care.

- Memory care.

- Nursing home care.

The downside is that you may never use it, and your policy price could increase in the future.

The price of a policy can be based on the following:

- Age: the younger you are, the lower your premium will be.

- The maximum a policy pays per day

- The maximum number of years a policy will pay

- Optional benefits, such as inflation protection

Option 2: Living benefits (life insurance)

Some individuals may consider leveraging their permanent/whole life insurance policy with an accelerated death benefit. This enables you to use a portion of your death benefit to cover long-term or other medical costs while you are alive. However, it’s essential to review your policy carefully to understand its limitations and consider adding riders if needed.

Another innovative option is a hybrid life insurance long-term care policy, which combines both life insurance and long-term care coverage. This provides more flexibility and can be a suitable alternative for those who wish to address both needs in one comprehensive policy.

It is essential to review your policy to determine what it includes and if you need to add riders.

- Check if the accelerated death benefit will increase your premium or if it is included in your premium.

- Check The triggers you need to get your accelerated death benefit approved. A common trigger is having a terminal illness. Check the triggers you can use for the accelerated death benefit.

Option 3: Retirement Savings

While using retirement savings to cover long-term care expenses eliminates the risk of paying for something you might not use, it could have adverse consequences. Depleting your retirement funds might leave your significant other or family members in financial hardship or lead to an unfortunate situation where you run out of money to support yourself in later years.

Option 3: Your family, friends, or go fund me

Unfortunately, many individuals find themselves unprepared for long-term care and end up relying on the support of their family, friends, or even resorting to crowdfunding. Research indicates that 64% of people who overlook planning for long-term care have to depend on the help of their family (Ahip.org, September 2016). However, this route is uncertain and does not guarantee that you will receive the care you need. This makes it unpredictable; you will depend on other people and won’t guarantee that you will get the care you need.

Option 4: Annuities

Funding long-term care costs can be achieved through annuities, which involve investing a lump sum with insurers. This generates a steady income that can be utilized for various expenses, including long-term care. The nature of the annuity chosen determines whether the income stream is consistent or variable. Although annuities are available for purchase at any age, they usually require a significant investment and may have a waiting period before payments begin..

Planning for long-term care can be tricky, but it is crucial. Feel free to schedule a meeting with one of our licensed financial planners if you need help creating a plan for long-term care or retirement. Identifying goals and objectives is critical to a successful retirement.