How Do I Sign Up for Medicare in 2026? A Complete Step-by-Step Guide

Approaching age 65? Understanding your health insurance options doesn’t have to be stressful. This breakdown will give you the clarity and confidence you need to take control of your healthcare.

Schedule a Medicare ReviewSkip to Section

Overview Eligibility Medicare Parts Real-World Scenarios Enrollment Periods How to Enroll Costs Coverage Options Mistakes FAQUnderstanding Medicare in 2026

Medicare is the federal health insurance program primarily designed for Americans aged 65 and older. While it is an incredible safety net, many people are surprised to learn that Medicare is not entirely free, nor does it cover 100% of your medical expenses. There are out-of-pocket costs like premiums, deductibles, and coinsurance that you need to plan for.

Because everyone’s health needs and financial situations are different, Medicare allows you to customize your coverage. You can choose to stick with the government-managed program or opt for a privately managed plan. Navigating these choices successfully comes down to knowing how the system works and—most importantly—when to sign up to avoid lifetime financial penalties.

Who Is Eligible for Medicare?

For most Americans, the magic number for Medicare eligibility is 65. However, there are a few different pathways to qualify:

- Age 65 and Older: You must be a U.S. citizen or a legal permanent resident who has lived in the country continuously for at least 5 years.

- Under Age 65 via Disability: If you have received Social Security Disability Insurance (SSDI) payments for 24 months, you are automatically eligible.

- Specific Medical Conditions: Individuals diagnosed with End-Stage Renal Disease (ESRD) requiring permanent kidney dialysis or a transplant, or those with Amyotrophic Lateral Sclerosis (ALS / Lou Gehrig’s disease), qualify for Medicare regardless of age.

The Four Building Blocks: Medicare Parts A, B, C & D

Medicare is organized into “Parts” that handle specific types of medical care. Understanding these terms makes comparing plans much easier.

Part A – Hospital Insurance

What it covers: Inpatient hospital stays, care in a skilled nursing facility, hospice care, and limited home health services.

The Cost: Free for most people, provided you or your spouse paid Medicare taxes while working for at least 10 years (40 quarters).

Part B – Medical Insurance

What it covers: Outpatient medical care, doctor visits, preventive services (like vaccines and screenings), medical equipment (wheelchairs, oxygen), and ambulance rides.

The Cost: Requires a monthly premium that adjusts annually based on your income ($202.90 baseline for 2026).

Part C – Medicare Advantage

What it covers: An alternative to Original Medicare. These are all-in-one private insurance plans that bundle Parts A, B, and usually D.

The Bonus: Often include extra benefits not found in standard Medicare, such as basic dental, vision, and fitness memberships.

Part D – Prescription Drugs

What it covers: Your outpatient prescription medications. These plans are run by private, government-approved insurance companies.

Important 2026 Update: Under new federal guidelines, total out-of-pocket prescription costs are capped at a maximum of **$2,000 per year**, completely protecting you from catastrophic pharmacy bills.

Which Scenario Fits Your Life Right Now?

The right time and way to enroll in Medicare changes completely based on what you are doing the year you turn 65. Find the profile below that best matches your situation:

Your Action Plan: This is a straightforward path. You should sign up for Medicare Parts A and B during your 7-month Initial Enrollment Period (IEP). If you are already collecting Social Security benefits, you’ll be enrolled automatically. If not, log onto SSA.gov three months before your birthday month to ensure your coverage kicks in on day one of your birth month.

Your Action Plan: If your employer has 20 or more employees, your group insurance is considered “primary.” You can choose to delay enrolling in Medicare Part B and Part D without facing penalties. Most people still choose to sign up for Part A because it is usually premium-free and can act as secondary coverage for hospital stays. (Be careful to stop all HSA contributions beforehand if choosing Part A).

Your Action Plan: Do not skip enrollment! For small businesses, Medicare legally becomes your primary health coverage the month you turn 65. If you do not sign up for Parts A and B, your workplace insurance can deny your medical claims completely, leaving you with the entire bill. Sign up during your normal IEP window.

Your Action Plan: Look at the size of your spouse’s employer. If they employ 20 or more people, you can safely remain on their plan and delay Part B. However, the moment your spouse stops working or leaves that group coverage, your 8-month Special Enrollment window opens to seamlessly transition onto Medicare.

When Can You Sign Up? Critical Enrollment Periods

Timing is everything with Medicare. Missing your designated window can cause a delay in your coverage and lead to lifetime late-enrollment penalties that increase your monthly premiums forever.

1. Initial Enrollment Period (IEP)

This is your primary window to sign up around your 65th birthday. It is a 7-month period that includes:

- The 3 months before the month you turn 65.

- The month of your 65th birthday.

- The 3 months after your birthday month.

2. Special Enrollment Period (SEP)

Are you planning to work past 65? If you have qualifying group health coverage through your current employer (or your spouse’s employer), you do not have to sign up at 65. When you finally decide to retire or leave that plan, you get an 8-month Special Enrollment Period to sign up for Medicare without any late penalties.

3. General Enrollment Period (GEP)

If you missed your Initial Enrollment Period and don’t qualify for a Special Enrollment Period, you can sign up between January 1 and March 31 each year. Your coverage will begin the first day of the month following your enrollment, meaning you no longer have to wait until July for coverage to take effect, though lifetime premium penalties may still apply.

4. Annual Enrollment Period (AEP)

Happening every year from October 15 to December 7. Once you are already in the Medicare system, this is your annual window to switch, drop, or add plans (like changing drug plans or moving between Original Medicare and Medicare Advantage) for the upcoming calendar year.

How to Sign Up for Medicare: Step-by-Step

- Check for Automatic Enrollment: If you are already receiving Social Security retirement benefits when you turn 65, you will be enrolled in Medicare Parts A and B automatically. Your Medicare card will simply show up in your mailbox about 3 months before your birthday.

- Apply via Social Security: If you are not yet taking Social Security benefits, you must manually apply. The fastest and easiest way is online at SSA.gov/medicare. You can also make an appointment at your local Social Security office or call them at 1-800-772-1213.

- Choose Your Coverage Pathway: Decide if you want to use Original Medicare (Parts A & B managed by the government) or Medicare Advantage (Part C managed by a private insurer).

- Secure Drug Coverage: If you choose Original Medicare, pick a standalone Part D prescription plan so your medications are covered.

- Evaluate a Medigap Policy: Look into Medicare Supplement Insurance (Medigap) if you stick with Original Medicare. It helps pay the remaining 20% of medical bills that Medicare leaves behind.

Understanding Medicare Costs (Official 2026 Figures)

While Medicare offers strong financial protection, you should map out these expected out-of-pocket costs for the 2026 calendar year:

| Medicare Component | Expected Cost Types | What to Know (2026 Metrics) |

|---|---|---|

| Part A (Hospital) | $0 Premium for most people. | Requires a $1,736 deductible per hospital benefit period before insurance covers structural care costs. |

| Part B (Medical) | $202.90 Standard Monthly Premium + 20% Coinsurance. | The annual Part B deductible is **$283**. Standard premiums are tied to your adjusted gross income via IRMAA surcharges if your 2024 MAGI exceeded $109,000 for single filers or $218,000 for joint filers. You typically owe 20% of outpatient doctor bills after meeting the deductible. |

| Part C (Advantage) | Varies widely by plan. | Many plans offer $0 or low monthly premiums, but you pay fixed network copays or coinsurance metrics as you receive medical care. |

| Part D (Prescriptions) | Monthly Premium + Tier Copays. | Premiums vary based on your specific medications. Under the newly implemented cap, your out-of-pocket pharmacy drug spending is legally capped at a strict **$2,000 maximum per calendar year**. |

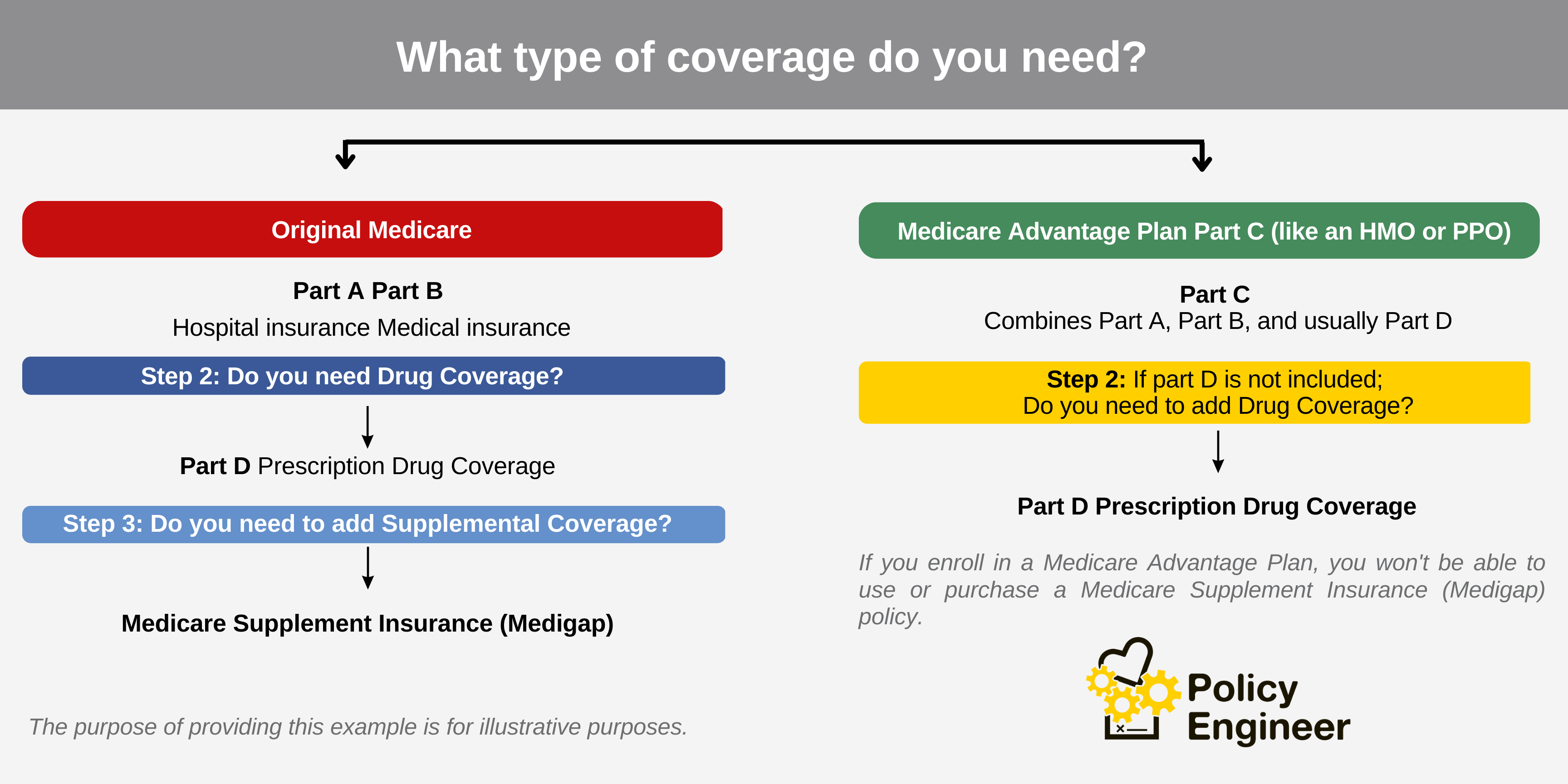

Medicare Coverage Options: Which Road Will You Choose?

You have two main pathways when setting up your coverage. They handle your medical care, doctor choices, and budgeting very differently:

Option 1: Original Medicare + Medigap

How it works: You use the federal government’s Medicare Parts A and B. You can see any doctor or visit any hospital in the United States that accepts Medicare—no networks and no referrals required.

To control your out-of-pocket exposure, you buy a private Medicare Supplement (Medigap) plan to cover your deductibles and co-insurance, along with a standalone Part D plan for prescriptions. This option has higher fixed monthly premiums but predictable, minimal costs when you visit the doctor.

Option 2: Medicare Advantage (Part C)

How it works: You opt out of the government-managed system and receive your Medicare benefits through an approved private insurance company (like an HMO or PPO network).

These plans usually feature very low or $0 monthly premiums and bundle your hospital, medical, and drug coverage together alongside extra perks like vision and dental care. However, you must stay within a local network of doctors, and you will pay copays out-of-pocket as you visit care providers up to a yearly maximum limit.

Common Medicare Mistakes to Avoid

- Assuming Everything is Free: Planning ahead for monthly premiums and deductibles keeps you from facing unexpected budget surprises.

- Missing the 7-Month IEP Window: Unless you have active employer coverage, missing this timeline results in delayed care and late fees that stay with you for life.

- Skipping Part D Drug Coverage: Even if you don’t take prescriptions today, you should enroll in a low-cost drug plan. Skipping it leaves you open to a permanent late-enrollment penalty if you need to add coverage down the road.

- Shopping by Premium Alone: A plan with a $0 premium might look great upfront, but make sure to check the doctor networks and drug formulary list to ensure your preferred medical providers and daily medications are actually covered.

Frequently Asked Questions (FAQ)

Do I have to sign up for Medicare if I am still working at age 65?

If your employer has 20 or more employees and your group health insurance is considered primary coverage, you can safely delay Part B and Part D without a penalty. If your company has fewer than 20 employees, you generally must enroll in Medicare at 65, as Medicare becomes the primary payer.

Can I change my Medicare plan layout if my health needs shift next year?

Yes. Every year during the Annual Enrollment Period (October 15 – December 7), you can safely switch between Original Medicare and Medicare Advantage, or swap out your prescription drug plans to better fit your changing health needs.

Does Medicare cover routine vision, dental, and hearing care?

Original Medicare (Parts A and B) does not cover routine eye exams, eyeglasses, dental cleanings, or hearing aids. If these coverages are important to you, you can find them bundled inside many private Medicare Advantage plans, or purchase standalone dental/vision policies.

What is the difference between Medicare and Medicaid?

This is a common point of confusion. Medicare is an entitlement program primarily based on age (65+) or specific severe disabilities, regardless of income. Medicaid is a joint federal and state program designed for individuals and families with limited income and resources. Some individuals qualify for both programs simultaneously and are referred to as “dual eligible.”

How much does Medicare cost monthly?

While Part A is free for most, Part B requires a base monthly premium of $202.90 in 2026. Higher income earners (individuals making over $109,000 single or $218,000 joint) will pay an additional fee called IRMAA (Income Related Monthly Adjustment Amount). Private options like Part C and Part D feature separate premiums baseline set by the specific plan you buy.

What is a Medigap plan, and do I really need it?

Medigap is private supplement insurance that works strictly alongside Original Medicare. Because standard Medicare only covers about 80% of your outpatient medical costs, a Medigap policy helps step in to pay the remaining 20% (including deductibles and copays). If you want predictable medical bills without dealing with restrictive network systems or doctor referrals, pairing Original Medicare with a Medigap plan is highly recommended.

Need Help Reviewing Your Medicare Options?

Schedule a free Medicare 101 review today.

Schedule ReviewMedicare.gov is the official U.S. government website for Medicare information.

Check out our Medicare 101 Handbook.

Learn more about Medicare, so you can make a confident decision and pick the best plan that fits your needs.

- The handbook Includes Parts A, B, C, and D of Medicare.

- What has changed in Medicare for the upcoming year

- Available plans

- Medicare plan buyer tips

- and much more!

- Medicare 101Understanding Your Medicare Plan Options (1)")

")